What Veterans in Silicon Valley Should Know About VA Home Loans

For many Veterans and active-duty service members, homeownership can feel out of reach right now.

That is understandable. In Silicon Valley, affordability is a real challenge. Home prices are higher than the national average, mortgage rates have shifted, and saving for upfront costs can feel like a long road.

But if you are eligible for a VA home loan, you may have more options than you realize.

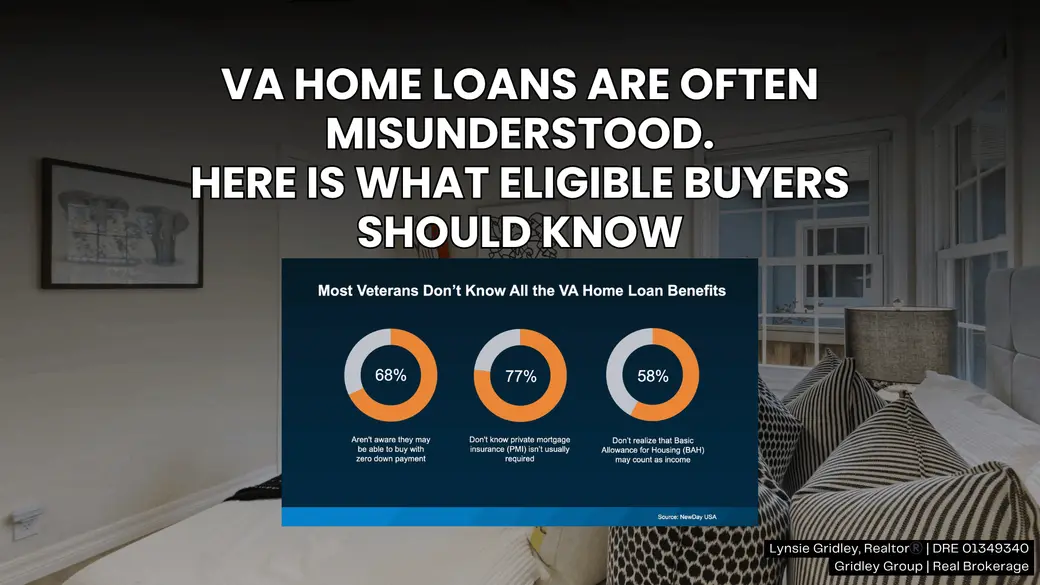

The VA home loan benefit has been helping Veterans, service members, and eligible surviving spouses buy homes for decades. The challenge is that many people do not fully understand what the benefit includes or how much it can help reduce the upfront cost of buying.

The VA Loan Is Not a Regular Mortgage

A VA-backed home loan is offered by private lenders, but part of the loan is guaranteed by the Department of Veterans Affairs. That guarantee can make lenders more comfortable offering favorable terms to eligible borrowers.

The VA says its home loan benefit may help eligible buyers purchase, build, improve, or refinance a home, but borrowers still need to meet lender requirements for credit, income, and occupancy.

That last part matters.

A VA loan is powerful, but it is not automatic approval. It is a benefit that can make the path easier if the borrower qualifies.

Benefit 1: You May Not Need a Down Payment

One of the biggest advantages of a VA home loan is the possibility of buying with no down payment.

The VA notes that lenders may require a down payment in some cases, but the VA itself does not require one for eligible borrowers with enough entitlement. The VA also says nearly 90 percent of VA-backed loans are made with no down payment.

In a high-cost market like Silicon Valley, that can be meaningful.

For many buyers, saving the down payment is one of the biggest obstacles. If a qualified Veteran or service member can buy with little or no money down, that may shorten the timeline to homeownership.

Benefit 2: Closing Costs May Be More Limited

Another part of the VA loan benefit is that certain closing costs are limited.

The VA explains that borrowers may still pay closing costs and may need to pay a VA funding fee, but the program is structured to help reduce costs compared with some traditional loan options.

For buyers, this matters because closing costs can add up quickly. Even when the down payment is low, buyers still need to plan for expenses like lender fees, escrow, title, prepaid taxes, and insurance.

A knowledgeable lender can help explain which costs apply and what may be limited under VA guidelines.

Benefit 3: You Typically Do Not Pay Monthly PMI

Private mortgage insurance, often called PMI, is commonly required on conventional loans when a buyer puts less than 20 percent down.

VA loans are different.

The VA says its home loan program does not require monthly mortgage insurance, and the Veterans Benefits Administration lists no PMI as one of the main pillars of the VA home loan benefit.

That can help reduce the monthly payment compared with other low down payment options.

For a Silicon Valley buyer, every monthly cost matters. Avoiding monthly PMI can make a noticeable difference in affordability.

What About the VA Funding Fee?

This is important.

VA loans often include a one-time VA funding fee. The VA explains that this fee helps lower the cost of the program for taxpayers because VA loans do not require down payments or monthly mortgage insurance.

Some Veterans may be exempt from the funding fee, including certain borrowers who receive VA compensation for a service-connected disability. The details depend on the borrower’s situation, so this is something to confirm with a VA-experienced lender.

BAH and BAS May Help Some Borrowers Qualify

For active duty service members or qualifying reservists, Basic Allowance for Housing and Basic Allowance for Subsistence may be considered as part of income by lenders.

This can matter because both allowances may help support mortgage qualification. Since they are generally nontaxable, lenders may evaluate them differently than regular taxable income, depending on the loan file and underwriting guidelines.

Because income qualification is lender-specific, this is another area where it is important to work with someone who understands VA lending.

What This Means in Silicon Valley

VA loans can be especially helpful in expensive markets because they may reduce some of the biggest upfront barriers to buying.

But buyers should still run the full numbers carefully.

In Silicon Valley, it is important to look at:

- Monthly payment

• Property taxes

• Homeowners insurance

• HOA dues, if applicable

• Commute and lifestyle needs

• Future plans for the home

• Total cash needed to close

A VA loan can open doors, but the right purchase still needs to fit your life and budget.

What Sellers Should Know About VA Buyers

Some sellers mistakenly assume VA buyers are weaker than conventional buyers.

That is not necessarily true.

A well-qualified VA buyer with strong lender support can be a very solid buyer. The key is understanding the loan, the appraisal process, and the buyer’s full financial picture.

For sellers in Silicon Valley, it is worth evaluating the strength of the whole offer rather than making assumptions based only on loan type.

Bottom Line

Many Veterans and service members are closer to homeownership than they think.

VA loans may offer no down payment, limited closing costs, and no monthly PMI for qualified buyers. But the details matter, and eligibility depends on service history, income, credit, entitlement, and lender requirements.

If you are active duty, a Veteran, or an eligible surviving spouse, it is worth speaking with a trusted VA experienced lender to understand what is possible.

And if you want help comparing homes, neighborhoods, and real monthly costs in Silicon Valley, I am always here as a resource.

Recent Posts

Her expert knowledge, negotiation, and marketing skills combined with her high level of commitment provide a framework for lasting relationships. Lynsie commits to “Bringing you the Best!”