Student Loans Are Back in the News. Do Not Assume They Put Homeownership Out of Reach

Student loans are back in the headlines, and if you are thinking about buying a home, that may feel discouraging.

Maybe you are wondering if your student loan payment will keep you from qualifying. Maybe you are worried about how it affects your credit. Or maybe you have already assumed that buying a home in Silicon Valley is not realistic until your student loans are fully paid off.

Here is the important thing to know.

Having student loans does not automatically prevent you from buying a home.

It does mean you need to understand how your loans affect your full financial picture, especially your monthly debt, credit history, savings, and loan qualification.

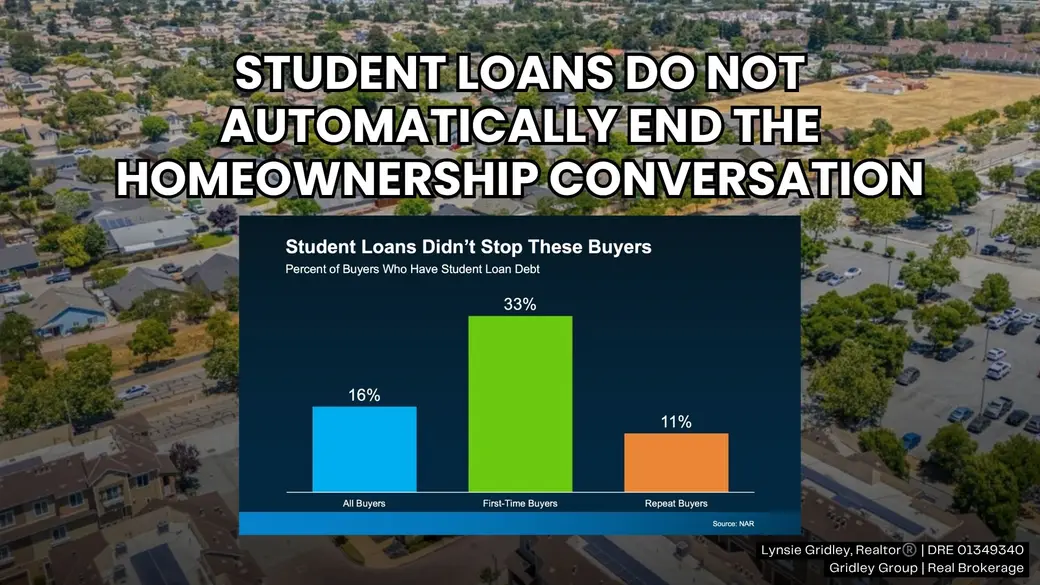

Student Loan Debt Can Delay Homeownership

Student loans are a real factor for many buyers.

The National Association of Realtors found that among recent home buyers, nearly one quarter of all buyers and 37 percent of first-time buyers had student loan debt. The typical amount was $30,000. NAR also reported that 51 percent of student loan holders said their debt delayed them from purchasing a home. (National Association of REALTORS®)

That explains why so many buyers feel stuck.

Student loans can make it harder to save for a down payment, build emergency reserves, reduce other debt, or feel confident about taking on a mortgage.

But delayed does not mean impossible.

What Lenders Actually Look At

Lenders do not usually look at student loan debt in isolation.

They look at the full file.

That includes income, credit score, monthly debt payments, assets, employment history, down payment, loan type, and the expected housing payment.

One of the most important numbers is your debt-to-income ratio. This compares your monthly debt obligations with your monthly income.

Student loans may be part of that calculation, but they are not the only part.

A buyer with student loans, high income, steady payment history, and manageable overall debt may still be able to qualify.

Payment History Matters

With student loans back in the news, payment history is especially important.

The U.S. Department of Education announced that Federal Student Aid resumed collections on defaulted federal student loans on May 5, 2025, after collections had been paused since March 2020. (U.S. Department of Education)

Federal Student Aid also explains that if action is not taken after a loan is placed in default, the default can be reported to major credit reporting agencies. (Federal Student Aid)

That matters because credit history affects mortgage options, interest rates, and loan approval.

If you are behind, in default, or unsure of your student loan status, address that before you begin the mortgage process. A lender can help you understand what needs to be resolved before applying.

Do Not Guess. Get the Loan Reviewed

One of the biggest mistakes buyers make is assuming they cannot qualify.

The better step is to speak with a trusted lender and have them review the actual numbers.

Ask them to look at:

- Your current student loan payment

- Whether your loan is in repayment, deferment, forbearance, delinquency, or default

- How the payment will be counted for the loan program you are considering

- Your total monthly debt

- Your credit profile

- Your savings and reserves

- Your down payment options

- Your full monthly housing payment

The answer may be better than you think. Or it may show you exactly what to work on before buying.

Either outcome is helpful.

Different Loan Programs May Treat Student Loans Differently

Mortgage programs can have different rules for calculating student loan payments.

Conventional, FHA, VA, and other loan types may not treat deferred loans, income-based repayment plans, and documented monthly payments the same way.

That is why online calculators can be misleading.

A calculator may not know how your specific student loan will be counted in underwriting.

A lender who understands student loans and mortgage guidelines can help you compare options and avoid surprises.

Student Loans May Affect Your Budget More Than Your Approval

Some buyers can technically qualify for a mortgage but still feel uncomfortable with the payment once student loans are included.

That distinction matters.

The goal is not simply to get approved.

The goal is to buy a home you can comfortably own.

In Silicon Valley, where housing costs are high, buyers should look carefully at the full monthly picture, including:

- Mortgage payment

- Property taxes

- Homeowners insurance

- HOA dues, if applicable

- Student loan payment

- Other monthly debts

- Utilities

- Maintenance

- Savings goals

A mortgage approval is the lender’s number. Your comfort number may be different.

What Buyers Can Do Now

If student loans are part of your financial picture, focus on preparation.

Start by confirming the exact status of each loan. Make sure your payments are current. Review your credit report. Avoid taking on new debt if you are planning to buy soon. Build savings for down payment, closing costs, and reserves.

Then ask a lender to compare different buying scenarios.

You may find that buying is possible now. You may also discover that paying down a credit card, adjusting your student loan repayment plan, or saving for a few more months puts you in a stronger position.

What Sellers Should Understand

This topic matters for sellers too.

A buyer with student loans is not automatically a weak buyer.

Many well-qualified buyers have student debt. What matters is whether they have lender approval, stable income, appropriate reserves, and a clear path to closing.

Sellers should evaluate the strength of the full offer, not make assumptions based on one part of the buyer’s financial life.

Bottom Line

Student loans are a real factor in homeownership, but they do not automatically put buying out of reach.

The key is understanding how your loans affect credit, debt-to-income ratio, savings, and monthly comfort.

If you have student loans and want to buy in Silicon Valley, do not assume the answer is no. Start with a lender review, look at the real numbers, and make a plan from there.

Recent Posts

Her expert knowledge, negotiation, and marketing skills combined with her high level of commitment provide a framework for lasting relationships. Lynsie commits to “Bringing you the Best!”