The Silicon Valley Housing Market Is Stronger Than the Headlines Suggest

There is no shortage of discouraging housing news right now.

Mortgage rates are elevated. Affordability is challenging. Homes may take longer to sell than they did a few years ago. And buyers and sellers are understandably wondering whether the market is becoming unstable.

But a slower market is not the same as a weak market.

The housing conditions of 2020 and 2021 were unusual. Extremely low mortgage rates, limited inventory, intense competition, and rapid price growth created a market that was never likely to last indefinitely.

Today’s market looks different because it is returning to more normal conditions.

And several important indicators show that the foundation remains stronger than many headlines suggest.

Homeowners Have a Significant Equity Cushion

One of the clearest signs of housing strength is homeowner equity.

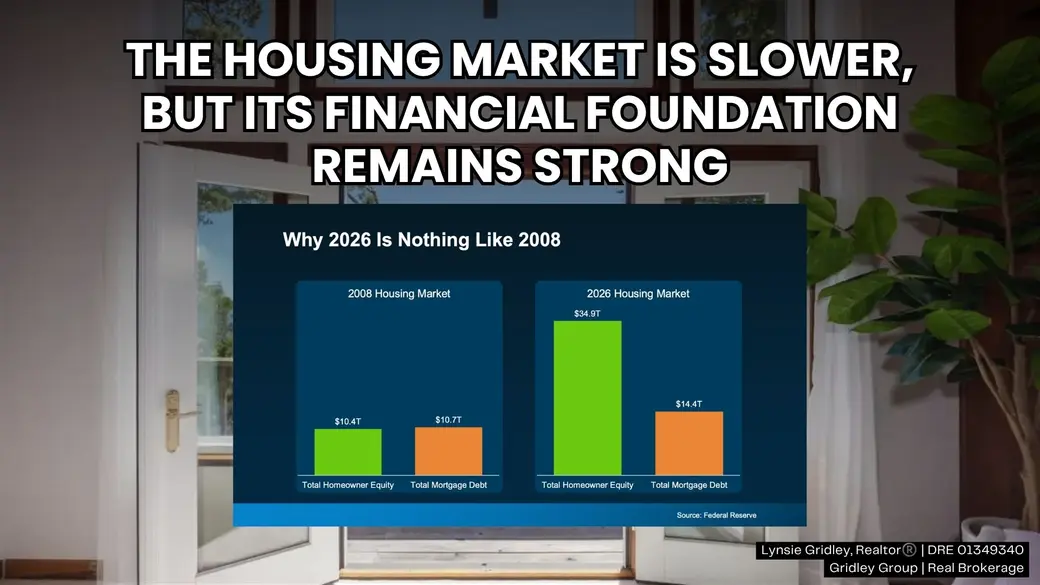

In 2008, total homeowner equity and mortgage debt were nearly equal. Many homeowners had little financial cushion, so job losses or falling prices quickly pushed borrowers into distress.

Today, homeowners collectively hold about $35 trillion in equity, substantially more than total mortgage debt.

That difference matters.

Equity gives homeowners options. They may be able to sell without bringing money to closing, use proceeds toward another purchase, or remain in place during a difficult financial period.

According to the article, homeowners who have owned for about five years have built approximately $180,000 in equity on average. Those who have owned for six to ten years have accumulated more than $340,000 on average. It also notes that about two-thirds of homeowners either own their homes outright or have more than 50 percent equity.

That is not the profile of a fragile housing market.

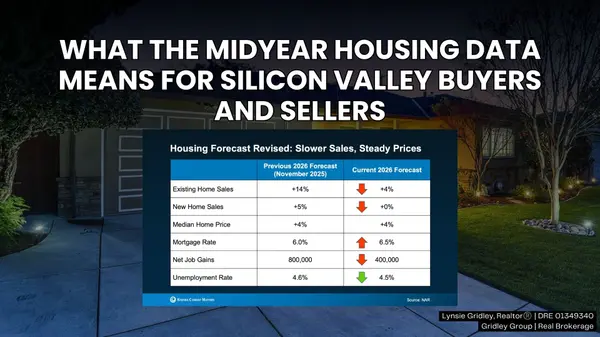

Low Existing Mortgage Rates Are Supporting Stability

More than half of active mortgages still have an interest rate below 4 percent, according to Federal Housing Finance Agency data referenced in the article.

Those low payments provide financial stability for many homeowners.

They also help explain why housing inventory remains limited. Owners with low mortgage rates may be reluctant to sell and take on a higher rate unless a move is truly necessary.

That limits the number of homes entering the market and helps prevent the type of oversupply that contributed to the last housing crash.

Foreclosures Remain Well Below Historic Levels

Foreclosure activity has increased slightly in some recent reports, but current volumes remain far below historic norms.

This is an important distinction.

An increase from an unusually low level can create an alarming headline without signaling widespread distress.

Most homeowners today have equity, fixed mortgage payments, and stronger loan structures than borrowers had before 2008. If financial challenges arise, many have options other than foreclosure.

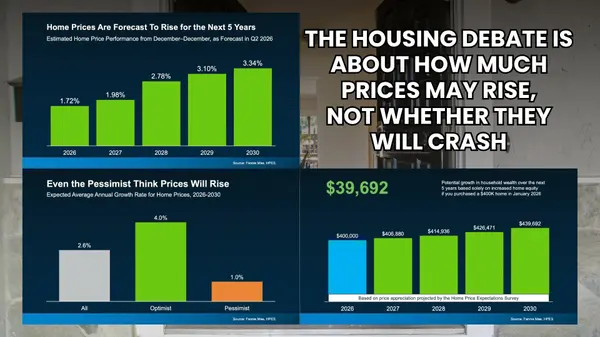

Prices Are Stabilizing, Not Collapsing

National home price growth has slowed to roughly 2 percent annually, according to the Redfin research referenced in the article.

That is very different from the rapid appreciation of the pandemic years.

But slower growth is not necessarily bad news.

More moderate appreciation can help wages gradually catch up, give buyers more time to make decisions, and create a healthier balance between buyers and sellers.

Some local markets may experience modest price declines. Others may continue to rise. The national picture is one of adjustment, not collapse.

Why Today Is Different From 2008

The last housing crash involved a combination of weak lending standards, risky mortgages, low homeowner equity, excessive construction, and widespread distressed selling.

Today’s market has a different foundation.

- Homeowners hold substantial equity

- Many borrowers have low fixed mortgage rates

- Lending standards are stronger

- Foreclosures remain historically low

- Housing supply remains limited in many areas

That does not mean the market is immune from challenges.

It means the current affordability problem is not the same as the financial instability that led to the last crash.

What This Means for Silicon Valley Buyers

For buyers, the stronger market foundation offers both reassurance and perspective.

Waiting for a widespread crash may not produce the opportunity some buyers expect.

If prices continue to grow gradually and inventory remains limited, waiting could mean facing a higher purchase price later. Lower mortgage rates could also bring more buyers back into the market and increase competition.

That does not mean you should buy before you are ready.

The better questions are:

- Can you comfortably manage the payment?

- Do you have adequate savings after closing?

- Does the home fit your expected timeline?

- Is the price supported by local market data?

- Does ownership make sense for your lifestyle?

A strong market foundation does not make every home a good purchase. Local analysis still matters.

What This Means for Silicon Valley Sellers

For sellers, today’s strength does not mean the market will do all the work.

Buyers are more selective and highly aware of monthly costs. Homes still need to be priced and presented thoughtfully.

The advantage is that most sellers are not operating from a position of distress.

Strong equity may allow a homeowner to negotiate strategically, prepare the property carefully, or plan the next move with greater flexibility.

Silicon Valley Is Still Highly Local

National indicators provide useful context, but Silicon Valley is made up of many smaller markets.

Conditions can vary by neighborhood, price range, property type, condition, and available inventory.

One home may receive several offers while another nearby property takes longer to sell.

That variation is not evidence that the market is broken. It is evidence that buyers are evaluating each property more carefully.

Bottom Line

The housing market is not as active or as fast as it was during the pandemic years.

But that does not make it fragile.

Strong homeowner equity, low existing mortgage rates, limited foreclosure activity, and moderate price growth all point to a market with a solid financial foundation.

If you are thinking about buying or selling in Silicon Valley, the best decision will come from looking beyond the headlines and understanding what the local data means for your specific plans.

Recent Posts

Her expert knowledge, negotiation, and marketing skills combined with her high level of commitment provide a framework for lasting relationships. Lynsie commits to “Bringing you the Best!”