Should Silicon Valley Sellers Help Pay a Buyer’s Closing Costs?

A few years ago, sellers had the leverage to say no to almost everything.

No repairs. No credits. No flexibility.

Today’s market is more balanced. Buyers have more choices, affordability remains challenging, and negotiation is once again a normal part of many transactions.

That does not mean sellers should agree to every request.

It means the best decision is not always the one that gives up the least. Sometimes, a carefully structured concession can help secure a qualified buyer, protect the sale, and support a better overall outcome.

One request sellers may encounter is help with the buyer’s closing costs.

What Are Buyer Closing Costs?

Closing costs are the expenses associated with completing a home purchase beyond the down payment.

They may include:

- Loan origination fees

- Appraisal and credit report fees

- Title and escrow services

- Government recording fees

- Prepaid property taxes and insurance

- Other lender and settlement charges

Freddie Mac advises buyers to generally prepare for closing costs equal to about 2 percent to 5 percent of the purchase price, although the actual amount depends on the loan, property, location, and transaction. (My Home)

On a $1 million Silicon Valley home, that broad estimate could represent $20,000 to $50,000.

That does not mean every buyer will pay that amount or that every cost may be covered by a seller. It shows why closing costs can be a meaningful affordability issue, even for a buyer who can manage the monthly mortgage payment.

Why Buyers Ask Sellers for Help

Many buyers are balancing several upfront expenses at once.

They may need funds for a down payment, inspections, moving expenses, reserves, repairs, and closing costs.

A buyer may be financially qualified for the mortgage but still want to preserve cash after closing. Others may prefer a closing cost credit because it offers more immediate help than a modest reduction in the purchase price.

The request is not automatically a warning sign. It is one part of the offer that should be considered alongside price, financing, contingencies, deposit, timing, and the buyer’s overall qualifications.

Seller Concessions Have Become Common

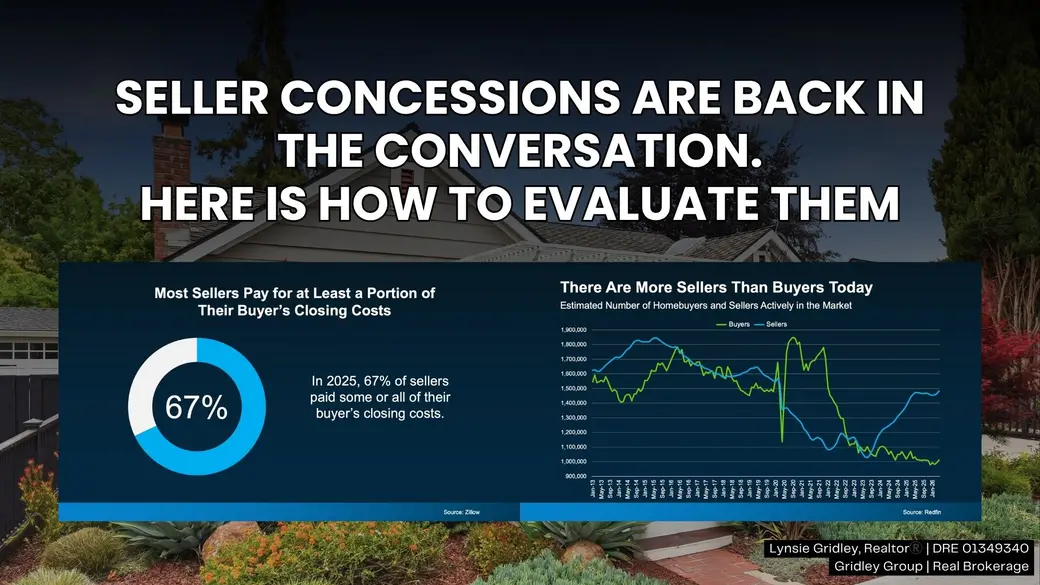

Seller-paid closing costs are no longer unusual nationally.

Zillow’s 2025 consumer housing research found that 67 percent of sellers reported paying some or all of the buyer’s closing costs in the offer they accepted. Of those sellers, 44 percent paid all and 23 percent paid some. (Zillow)

That does not mean 67 percent of Silicon Valley sellers should offer a credit.

National statistics cover many different markets. In some areas, buyers hold considerable negotiating power. In other areas, including competitive parts of the Bay Area, sellers may still receive multiple offers and have little reason to offer concessions.

The local market determines the leverage.

Why Market Conditions Matter

Redfin reported that there were approximately 47 percent more sellers than buyers nationally in April 2026. That gave buyers meaningful negotiating power across much of the country, although the balance varied substantially by region and metropolitan area. (Redfin)

Silicon Valley cannot be treated as one uniform market either.

A well-prepared home in a sought-after neighborhood may still attract strong competition. Another home at a higher price point, in less polished condition, or with more competing inventory may require greater flexibility.

The question is not simply whether concessions are common nationally.

The question is what is needed to sell your particular home under current local conditions.

When Paying Closing Costs May Make Sense

A closing cost credit may be worth considering when:

- Your home has been on the market longer than expected

- You have had showings but limited offer activity

- Several similar homes are competing for the same buyers

- The buyer is otherwise well qualified

- The credit helps preserve an acceptable sale price

- The request arises after inspections and helps keep the transaction together

- Your timing is more important than holding firm on every term

The value of a concession should always be measured against the cost of not reaching an agreement.

If declining a reasonable request causes the home to return to the market, the seller may face additional mortgage payments, taxes, insurance, maintenance, staging costs, and uncertainty.

Sometimes, a defined credit is the less expensive choice.

A Credit May Be More Useful Than a Price Reduction

A buyer may benefit more from help with closing costs than from a similar reduction in price.

A modest price reduction is spread across the life of the loan and may create only a small change in the monthly payment.

A closing cost credit can reduce the amount of cash the buyer needs at closing. Depending on the loan and lender approval, it may also be used for eligible costs such as discount points or a rate buydown.

The structure must comply with the buyer’s loan program, lender guidelines, appraisal requirements, and the purchase agreement.

A credit the buyer cannot fully use does not provide additional benefit, so the amount should be confirmed with the lender before the terms are finalized.

Concessions Are Not Unlimited

Seller concessions are subject to financing rules.

The permitted amount can depend on the loan program, down payment, occupancy, and how the credit is used. A seller generally cannot simply give the buyer unrestricted cash through the transaction.

The credit must be documented and approved as part of the loan and closing process.

This is one reason buyers, sellers, agents, escrow professionals, and lenders need to coordinate closely.

Other Concessions Sellers Can Consider

Paying closing costs is not the only way to add value.

Depending on the buyer’s priorities, a seller might consider the following:

- A credit for agreed repairs

- A home warranty

- Included appliances

- Flexibility on the closing date

- Additional time for the buyer to move

- A seller rent back when it benefits both parties

- A credit toward an eligible mortgage rate buydown

The most effective concession is the one that solves the buyer’s concern without undermining the seller’s larger goal.

Evaluate the Net Proceeds, Not Just the Headline Price

Sellers often focus on the offered price first.

But the highest price does not always produce the strongest net result.

An offer should be evaluated based on:

- Purchase price

- Requested credits

- Repair expectations

- Financing strength

- Appraisal risk

- Contingencies

- Closing timeline

- Probability of completion

- Estimated net proceeds

An offer with a slightly lower price and cleaner terms may be stronger than a higher offer carrying a large credit, uncertain financing, and greater contingency risk.

Likewise, a strong offer with a reasonable closing cost request may still deliver the best overall result.

What This Means for Silicon Valley Sellers

Silicon Valley remains highly local.

Negotiating conditions can change from one neighborhood to another and from one price range to another.

A seller in a competitive segment may have little reason to offer closing cost assistance. A seller facing more inventory, longer market times, or a narrower buyer pool may benefit from using a concession strategically.

Flexibility is not the same as weakness.

The goal is to understand where to compromise, where to protect your position, and how each term affects your final result.

Bottom Line

You do not need to agree to every request from a buyer.

But automatically rejecting closing cost assistance may not always serve your goals.

In today’s Silicon Valley market, the right concession can sometimes attract a stronger offer, protect a transaction, or help you move forward on your preferred timeline.

The decision should be based on local competition, the strength of the buyer, your expected net proceeds, and what matters most to you.

Recent Posts

Her expert knowledge, negotiation, and marketing skills combined with her high level of commitment provide a framework for lasting relationships. Lynsie commits to “Bringing you the Best!”