Are Adjustable Rate Mortgages a Smart Option in Silicon Valley Right Now

If you have been home shopping in Silicon Valley, you have likely felt the pressure of affordability.

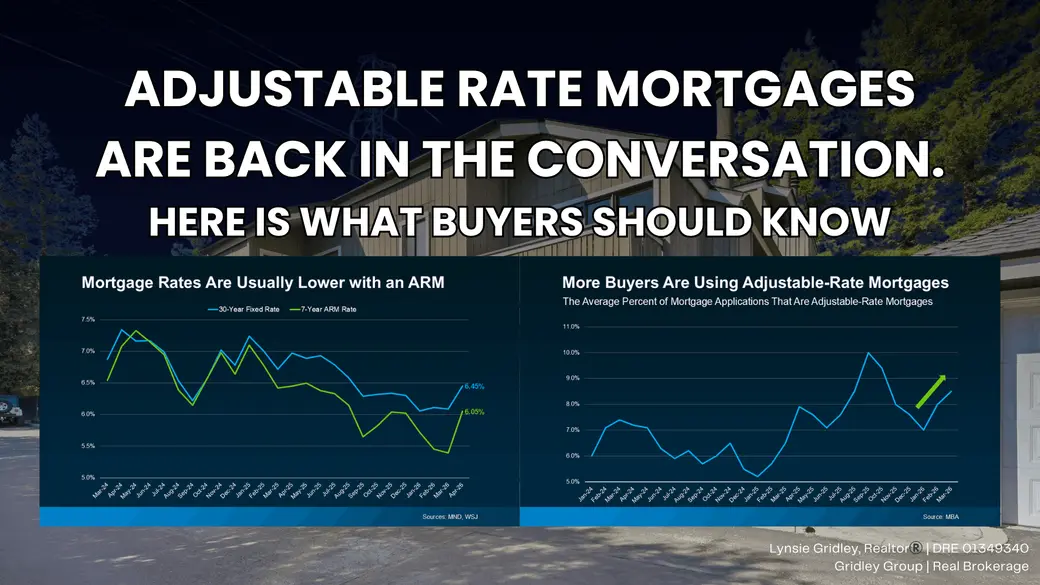

With mortgage rates still elevated compared to recent years, many buyers are exploring different ways to make the numbers work. One option that is getting more attention again is the adjustable rate mortgage, often called an ARM.

Before you go that route, it is worth understanding how it works and whether it fits your plan.

What Is an Adjustable-Rate Mortgage

An adjustable-rate mortgage starts with a fixed interest rate for a set period of time. After that, the rate can adjust periodically based on market conditions.

By contrast, a fixed-rate mortgage keeps the same interest rate for the life of the loan, which means your base monthly payment stays consistent.

With an ARM, your payment could go up or down after the initial fixed period ends.

Why Buyers Are Considering ARMs

The main reason buyers are looking at ARMs right now is simple. Lower initial rates.

In many cases, an ARM offers a lower starting interest rate than a traditional 30-year fixed loan. That can translate into a lower monthly payment or allow a buyer to qualify for a higher purchase price.

In a market like Silicon Valley, where home prices are higher, even a modest difference in monthly payment can make a meaningful impact.

Why This Is Not 2008

It is natural to feel cautious when hearing about ARMs again.

But today’s lending environment is very different from the period leading up to 2008. Borrowers are more carefully qualified, and lenders evaluate whether buyers can handle potential payment increases.

The increase in ARM usage today reflects buyers adapting to affordability challenges, not a return to risky lending practices.

The Trade-Off to Consider

An ARM can be a helpful tool, but it comes with trade-offs.

Once the fixed period ends, your interest rate can adjust. If rates are higher at that time, your monthly payment could increase.

There is also no guarantee that rates will drop in the future, which means refinancing may not always be an option.

When an ARM May Make Sense

An ARM may be worth considering if:

You plan to move or sell before the adjustment period begins

You expect your income to grow over time

You want lower upfront payments and are comfortable with some future uncertainty

When to Be More Cautious

You may want to think carefully if:

You plan to stay in the home long term

You prefer predictable monthly payments

You are already stretching your budget

Bottom Line

Adjustable-rate mortgages are not right for everyone, but they can be a useful option in the right situation.

In Silicon Valley, where affordability plays a big role, understanding all your financing options is key.

If you want to talk through how this fits into your home search and connect with a trusted lender, I am always here to help.

Recent Posts

Her expert knowledge, negotiation, and marketing skills combined with her high level of commitment provide a framework for lasting relationships. Lynsie commits to “Bringing you the Best!”